From optimal to investable: implementing a portfolio of ETFs, part 2

Note: A Google Sheets spreadsheet corresponding to this story is available here.

In the previous article of this series, the difference between an optimal portfolio¹ and an investable portfolio² was illustrated with a portfolio of ETFs.

It was also established that this difference is a problem that only plagues small portfolios.

Diversified investable portfolios

Unfortunately, large portfolios are subject to other problems, and in particular to the problem of concentration risk.

For example, if you are implementing a 60/40 Portfolio strategy — with 60% of your portfolio invested in US stocks and 40% of your portfolio invested in US bonds — , you might be using the standard IVV and TLT ETFs from the ETF provider iShares.

Problem is, if you were to invest several million dollars in such a portfolio, you would actually be trusting only one ETF provider with all these dollars!

Graphical example below, for a 2,500,000 USD portfolio:

Such a portfolio presents a very high concentration risk in terms of ETF providers.

Hopefully, there is a simple way to alleviate this risk, which is to incorporate ETFs from other ETF providers:

- Alternatives to IVV: SPY (SPDR), VOO (Vanguard)

- Alternatives to TLT: SPTL (SPDR), VGLT (Vanguard)

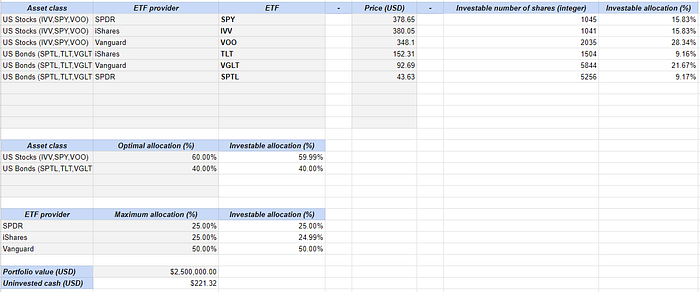

Graphical example below, for an ETF provider-diversified 2,500,000 USD portfolio:

While as “close” to the optimal 60/40 Portfolio as its 100% iShares sibling, this investable portfolio bears far less concentration risk in terms of ETF providers thanks to its perfect diversification among 3 different ETF providers.

Mathematical formulation of the problem

In real life, the problem of minimizing concentration risk in a large portfolio of ETFs is more complex than the toy example above:

- While it might be desirable to diversify ETF providers, an ETF tracking a specific asset class might only available from a single ETF provider

- In addition to diversifying ETF providers, it might also be desirable to diversify synthetic v.s. physical ETFs³, or to diversify distributing v.s. accumulating ETFs⁴, or to diversify other intrinsic ETFs characteristics

- Going beyond intrinsic ETFs characteristics, it might also be desirable to diversify brokerage firms⁵, currencies exposition, etc.

In all generality, the problem of minimizing concentration risk in an investable portfolio can be formalized as a mathematical optimization problem whose aim is to

compute the investable portfolio which exhibits the minimum deviation⁶ from the optimal portfolio while best⁷ taking into account concentration risk constraints.

Computational solution

As in the previous article of this series, solving this optimization problem is computationally very challenging, so that the usage of heuristics is required to compute a good enough solution within a reasonable time frame.

Such a heuristic, using a stochastic optimization algorithm, is provided by Portfolio Optimizer through a Web API.

Re-using the example above of a 60/40 Portfolio of 2,500,000 USD, an investable portfolio satisfying maximum ETF providers concentration constraints can easily be computed by Portfolio Optimizer:

- Through cURL:

curl "https://api.portfoliooptimizer.io/v1/portfolio/construction/investable" \

-H "Content-Type: application/json" \

-d '{ "assets": 6,

"assetsGroups": [[1,2,3],[4,5,6],[1,6],[2,4],[3,5]],

"assetsGroupsWeights": [0.6,0.4,null,null,null],

"maximumAssetsGroupsWeights:" [null,null,0.25,0.25,0.50],

"assetsPrices": [378.65,380.05,348.1,152.31,92.69,43.63],

"portfolioValue": 2500000 }'{

"assetsPositions":[1045,1041,2035,1504,5844,5256],

"assetsWeights":[0.1582,0.1584,0.2833,0.0916,0.2166,0.0916]

}

- Through a Google Sheets integration

This concludes this 2-part series on the computation of investable portfolios of ETFs.

[1]: Made of real-valued weights, like 86.42%

[2]: Made of integer-valued number of shares, like 5 shares

[3]: The underlying risks are not the same

[4]: Typically, for taxes reasons

[5]: Typically, to reduce the risk of a single broker going bankrupt, or the risk of having a portfolio fully or partially frozen for whatever reason linked to a single broker (technical maintenance, trading restrictions suddendly imposed like Robinhood did with the GME stock…)

[6]: An example of measure of the deviation between two portfolios is the Euclidean distance between the two portfolios real-valued weights

[7]: The word “best” is important here, because — mathematically — an investable portfolio satisfying all the risk concentration constraints might not exist.

Disclaimer

Under no circumstances does any information on this story represent a recommendation to buy, sell, or hold any security.

None of the content of this story is guaranteed to be correct, and anything shown should be subject to independent verification.

You, and you alone, are solely responsible for any investment decisions that you make.